.jpg) 1 hour ago

3

1 hour ago

3

Article content

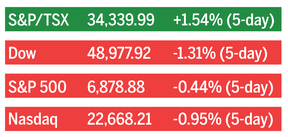

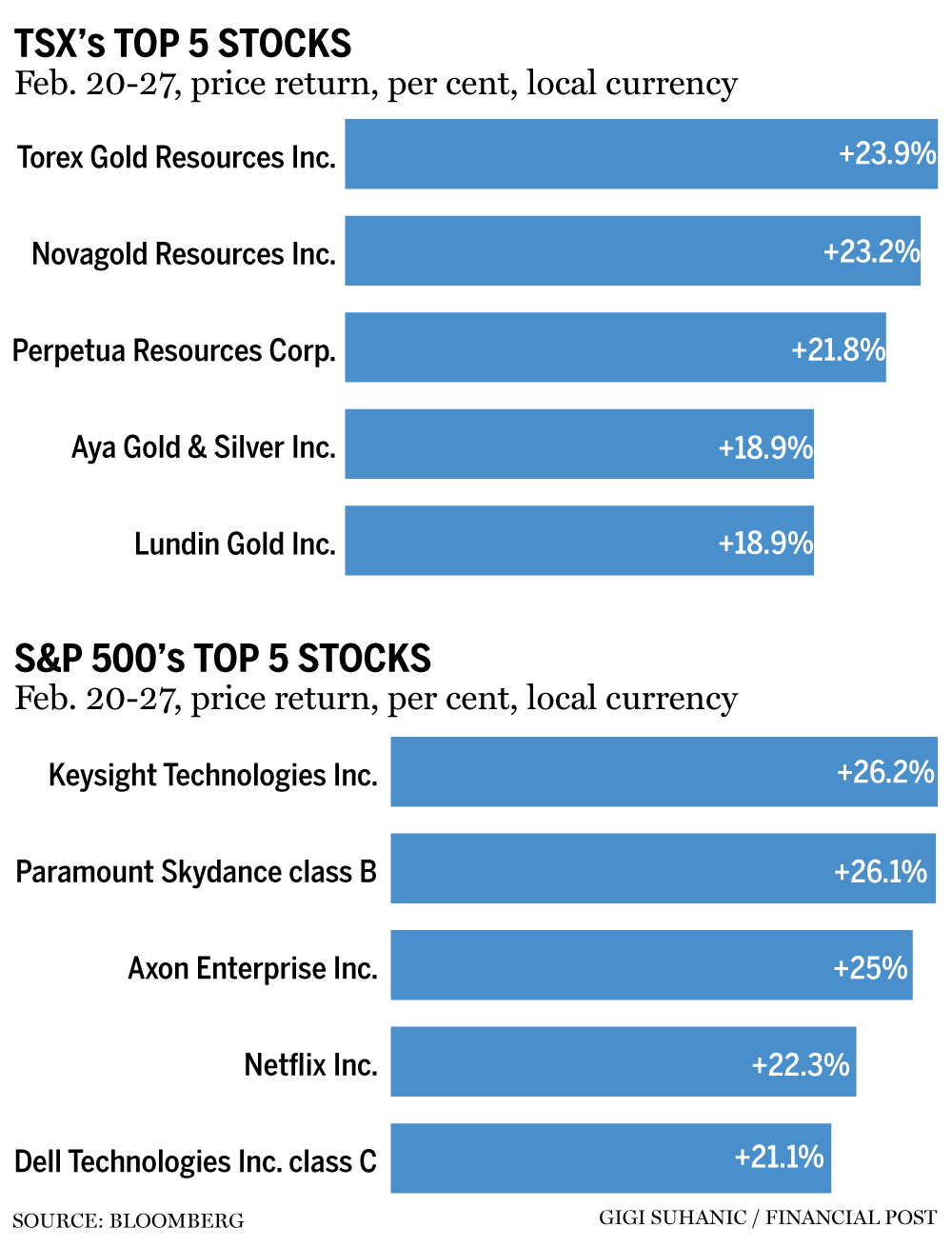

Which Big Bank price targets moved the most post-earnings, why National Bank says it’s time to lean into dividend payers and more from The Week in Stocks.

![]()

THIS CONTENT IS RESERVED FOR SUBSCRIBERS ONLY

Subscribe now to read the latest news in your city and across Canada.

- Exclusive articles from Barbara Shecter, Joe O'Connor, Gabriel Friedman, and others.

- Daily content from Financial Times, the world's leading global business publication.

- Unlimited online access to read articles from Financial Post, National Post and 15 news sites across Canada with one account.

- National Post ePaper, an electronic replica of the print edition to view on any device, share and comment on.

- Daily puzzles, including the New York Times Crossword.

SUBSCRIBE TO UNLOCK MORE ARTICLES

Subscribe now to read the latest news in your city and across Canada.

- Exclusive articles from Barbara Shecter, Joe O'Connor, Gabriel Friedman and others.

- Daily content from Financial Times, the world's leading global business publication.

- Unlimited online access to read articles from Financial Post, National Post and 15 news sites across Canada with one account.

- National Post ePaper, an electronic replica of the print edition to view on any device, share and comment on.

- Daily puzzles, including the New York Times Crossword.

REGISTER / SIGN IN TO UNLOCK MORE ARTICLES

Create an account or sign in to continue with your reading experience.

- Access articles from across Canada with one account.

- Share your thoughts and join the conversation in the comments.

- Enjoy additional articles per month.

- Get email updates from your favourite authors.

THIS ARTICLE IS FREE TO READ REGISTER TO UNLOCK.

Create an account or sign in to continue with your reading experience.

- Access articles from across Canada with one account

- Share your thoughts and join the conversation in the comments

- Enjoy additional articles per month

- Get email updates from your favourite authors

Sign In or Create an Account

or

Article content

Stock of the week: Enerflex Ltd.

Article content

Article content

Shares of Enerflex Ltd. (EFX:TSX) surged nearly 18 per cent on Thursday, placing it among the top 10 gainers on the S&P/TSX composite index this week after the company beat analysts’ estimates for earnings before interest, taxes, depreciation and amortization (EBITDA) by 15 per cent, TD Cowen analyst Aaron MacNeil said. As a result, he “meaningfully” hiked his price target for Enerflex to $39 from $28 while reconfirming it as his top pick in the energy services sector. Shares closed Friday at $30.61, with the stock up nearly 48 per cent this year. MacNeil said he raised his EBITDA estimates for 2026 and 2027 by seven per cent and 10 per cent, respectively. He also said he believes the shares are undervalued compared with peers and merit a “premium valuation” based on the “growing power demand opportunity and to reflect broader energy sector multiple expansion.” Enerflex will likely hold an investor day in the spring and the analyst thinks that will act as a “catalyst” for the stock. The average 12-month price target based on nine analysts tracked by Bloomberg is $34.35.

Article content

Article content

Keeping score

Article content

Article content

Article content

By signing up you consent to receive the above newsletter from Postmedia Network Inc.

Article content

Big 6 bank price targets get a rethink post-earnings

Article content

Canada’s Big Six banks just closed out a fourth-quarter earnings season that was generally well received by Bay Street. The next question for investors is where do the stocks, which helped propel the S&P/TSX composite to a robust gain in 2025, go from here? In a note to investors, RBC Capital Markets analyst Darko Mihelic raised his price estimate for Toronto-Dominion Bank (TD:TSX) to $148 from $133 on a “solid” quarter after results came in stronger than expected across multiple sectors. TD shares closed Friday at $132.88. In this low loan-growth environment, Mihelic, in a separate note, said he likes Canadian Imperial Bank of Commerce (CM:TSX), which he described as “better positioned” to manage those challenges. He increased earnings estimates for CIBC and hiked his price target to $158 from $134. CIBC shares closed Friday at $137.79. At the Bank of Montreal (BMO:TSX), pre-provision (or before setting aside funds for loan losses), pre-tax earnings were better than expected on “solid revenues and cost discipline,” Mihelic said. Signs of slight worsening in Canadians’ credit quality “have been seen at all banks so far, but outlooks remain positive,” he said. The analyst raised his price for BMO to $219 from $178. BMO shares closed Friday at $196.31. Mike Rizvanoic, an analyst at Scotia Capital Markets, “modestly” moved up his price target for Royal Bank of Canada (RY:TSX) to $247 from $242. He said RBC’s lagging share performance compared with its peers on earnings day likely reflected lower increase in earnings per share compared with the whole group and a “tepid approach” to share buybacks. RBC closed Friday at $228.07. On National Bank of Canada (NA:TSX), “we believe NA put out a very good set of results this quarter,” Rizvanovic said, pointing to a slew of reasons, including a “big beat” in the Canadian personal and commercial loans sector. He raised his price target for National to $202 from $188. Shares closed Friday at $190.37. Finally, TD Cowen analyst Mario Mendonca maintained his price target of $112 for Bank of Nova Scotia (BNS:TSX). Shares closed Friday at $103.44. He said the challenge for Scotiabank is to improve loan growth, especially corporate and commercial and investment banking.

Article content

Article content

Article content

National Bank’s dividend payer picks could take the sting out of volatility

Article content

National Bank Capital Markets said investors might be in the mood for a break from the ongoing market volatility, and it has updated its list of preferred dividend payers for the first half of 2026. “With continued macroeconomic uncertainty and elevated market volatility, dividend stocks could regain favour with investors,” National Bank Research said in a note. To be included on the list, companies need a yield of five per cent or greater, a decent chance of the payout growing and a positive outlook. For the first half, the portfolio of 23 companies has an average yield of 4.8 per cent — lower due to rising share prices — and an average payout ratio of 62.8 per cent. The top five companies based on dividend yield are Automotive Properties REIT (APRU:TSX) with a yield of 7.2 per cent, Alaris Equity Partners Income Trust (AD/U:TSX) at 6.6 per cent, Gibson Energy Inc. (GEI:TSX) at 6.1 per cent, RioCan REIT (REI/U:TSX) at 5.9 per cent and Crombie REIT (CRR:TSX) at 5.6 per cent. In the second half of last year, National’s list returned 25.4 per cent — 2.1 per cent income and 23.3 per cent share price appreciation — while the S&P/TSX composite returned 1.4 per cent in income and 15.8 per cent in price over the same period.

English (US)

English (US)