.jpg) 11 hours ago

3

11 hours ago

3

Article content

(Bloomberg) — Beneath the calm surface of the US corporate bond market, there are worrying signs about companies that could lose their investment-grade status.

![]()

THIS CONTENT IS RESERVED FOR SUBSCRIBERS ONLY

Subscribe now to read the latest news in your city and across Canada.

- Exclusive articles from Barbara Shecter, Joe O'Connor, Gabriel Friedman, and others.

- Daily content from Financial Times, the world's leading global business publication.

- Unlimited online access to read articles from Financial Post, National Post and 15 news sites across Canada with one account.

- National Post ePaper, an electronic replica of the print edition to view on any device, share and comment on.

- Daily puzzles, including the New York Times Crossword.

SUBSCRIBE TO UNLOCK MORE ARTICLES

Subscribe now to read the latest news in your city and across Canada.

- Exclusive articles from Barbara Shecter, Joe O'Connor, Gabriel Friedman and others.

- Daily content from Financial Times, the world's leading global business publication.

- Unlimited online access to read articles from Financial Post, National Post and 15 news sites across Canada with one account.

- National Post ePaper, an electronic replica of the print edition to view on any device, share and comment on.

- Daily puzzles, including the New York Times Crossword.

REGISTER / SIGN IN TO UNLOCK MORE ARTICLES

Create an account or sign in to continue with your reading experience.

- Access articles from across Canada with one account.

- Share your thoughts and join the conversation in the comments.

- Enjoy additional articles per month.

- Get email updates from your favourite authors.

THIS ARTICLE IS FREE TO READ REGISTER TO UNLOCK.

Create an account or sign in to continue with your reading experience.

- Access articles from across Canada with one account

- Share your thoughts and join the conversation in the comments

- Enjoy additional articles per month

- Get email updates from your favourite authors

Sign In or Create an Account

or

Article content

The first full week of the year has been one of the busiest for US corporate debt sales on record, and risk premiums stayed low even amid heavy issuance. But the amount of bonds teetering on the brink of junk surged last year, according to JPMorgan Chase & Co.

Article content

Article content

Article content

Around $63 billion of US corporate bonds in the high-grade universe have a high-yield rating from one bond grader, a BBB- rating from others, and at least one negative outlook, according to the bank’s review based on ratings for debt in its high-grade US index. That figure was $37 billion at the end of 2024, JPMorgan strategists wrote.

Article content

By signing up you consent to receive the above newsletter from Postmedia Network Inc.

Article content

“As companies continue to refinance debt, the pressure on their balance sheets from rising interest expense is growing,” said Nathaniel Rosenbaum, a US high-grade credit strategist at JPMorgan. “That, in turn, does put a little bit more ratings pressure on weaker credits.”

Article content

JPMorgan doesn’t anticipate market turmoil anytime soon. Demand from investors is still strong, and earnings will probably be relatively strong in the coming weeks, leaving spreads relatively rangebound.

Article content

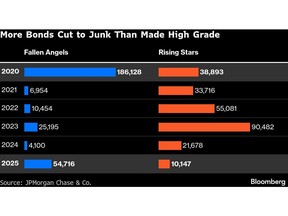

But there are still risks in credit. About $55 billion of US corporate bonds migrated from investment-grade to junk status in 2025, becoming “fallen angels,” according to JPMorgan. That far exceeds last year’s $10 billion of “rising stars,” or firms elevated to high-grade. And the trend is set to continue, the strategists say.

Article content

Article content

BBB- debt is just 7.7% of JPMorgan’s US high-grade corporate index, a record low share. But a relatively high amount of debt is susceptible to being cut to junk. Companies typically see their spreads blow out when they lose their high-grade status, as the universe of junk bond investors is much smaller in dollar terms than investment-grade.

Article content

There are reasons to be a little more concerned about credit risk now: Broad measures of indebtedness have been creeping higher relative to earnings, fueled by rising yields after the pandemic, a flood of spending on artificial intelligence, and acquisitions.

Article content

“If you look underneath the hood there are underlying signs of weakening in credit profiles,” said Zachary Griffiths, head of US investment grade and macro strategy at CreditSights Inc.

Article content

But in the near term, demand for bonds has been strong. And fiscal stimulus from some provisions of the One Big Beautiful Bill Act could help keep consumer sentiment “a little more buoyant,” Griffiths said.

Article content

Generally, money manager have been less worried about credit risk for months. Investment-grade spreads have spent much of this week averaging 0.78 percentage point, or 78 basis points, and haven’t risen above 85 basis points since June, according to Bloomberg index data. The mean for the last decade is closer to 116 basis points.

English (US)

English (US)