.jpg) 1 hour ago

4

1 hour ago

4

Article content

(Bloomberg) — Even before the Iran war, Fidelity International portfolio manager Mike Riddell was skeptical of the view that global price pressures were subsiding. His contrarian bet — that inflation was set to rise — is now paying off handsomely.

![]()

THIS CONTENT IS RESERVED FOR SUBSCRIBERS ONLY

Subscribe now to read the latest news in your city and across Canada.

- Exclusive articles from Barbara Shecter, Joe O'Connor, Gabriel Friedman, and others.

- Daily content from Financial Times, the world's leading global business publication.

- Unlimited online access to read articles from Financial Post, National Post and 15 news sites across Canada with one account.

- National Post ePaper, an electronic replica of the print edition to view on any device, share and comment on.

- Daily puzzles, including the New York Times Crossword.

SUBSCRIBE TO UNLOCK MORE ARTICLES

Subscribe now to read the latest news in your city and across Canada.

- Exclusive articles from Barbara Shecter, Joe O'Connor, Gabriel Friedman and others.

- Daily content from Financial Times, the world's leading global business publication.

- Unlimited online access to read articles from Financial Post, National Post and 15 news sites across Canada with one account.

- National Post ePaper, an electronic replica of the print edition to view on any device, share and comment on.

- Daily puzzles, including the New York Times Crossword.

REGISTER / SIGN IN TO UNLOCK MORE ARTICLES

Create an account or sign in to continue with your reading experience.

- Access articles from across Canada with one account.

- Share your thoughts and join the conversation in the comments.

- Enjoy additional articles per month.

- Get email updates from your favourite authors.

THIS ARTICLE IS FREE TO READ REGISTER TO UNLOCK.

Create an account or sign in to continue with your reading experience.

- Access articles from across Canada with one account

- Share your thoughts and join the conversation in the comments

- Enjoy additional articles per month

- Get email updates from your favourite authors

Sign In or Create an Account

or

Article content

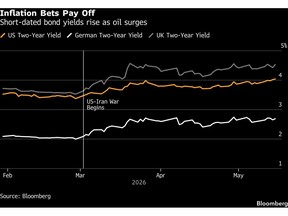

Months ago, he bought inflation swaps in the US and UK, essentially protection against hotter-than-forecast inflation. That’s because he saw inflation as a potent risk that bond markets — and most of his peers — were underpricing even before the Iran war sent oil prices soaring past $100 a barrel. That bet has helped returns on his two Strategic Bond Funds to surpassed more than 90% of peers, data compiled by Bloomberg show.

Article content

Article content

Article content

“There was absolutely no risk of a Middle East conflict priced into rates, given the multiple cuts that global investors were expecting,” Riddell said in an interview.

Article content

By signing up you consent to receive the above newsletter from Postmedia Network Inc.

Article content

“We positioned the fund to be long inflation, short rates short credit risk, short risk assets.”

Article content

He continues to holds the inflation swaps, though he’s trimmed the positions slightly.

Article content

Read: Global Bond Selloff Worsens as Rising Oil Prices Spook Investors

Article content

It’s proved to be the right call from Riddell and his team, which includes Ravin Seeneevassen and Tim Foster. Soaring oil prices since the war have fed into inflation expectations and whipsawed global bond markets, while money markets have reversed gear to price rate hikes across much of the developed world. That’s resulted in losses for any investor who was positioned for lower rates.

Article content

As of Friday, swaps markets are pricing at least two rate increases in the UK by year-end, a dramatic pivot from having bet on two cuts less than three months ago. For the Federal Reserve, pricing for any cut has been wiped out in favor of a hike in a year’s time, while the European Central Bank is expected to deliver three increases this year, starting next month.

Article content

Article content

Those expectations have lifted two-year US Treasury yields to the highest in more than a year, while German and UK equivalents have also soared. Borrowing costs have risen across the world this week, amid intensifying fears that war-driven inflation will force central banks to pursue higher interest rates.

Article content

Riddell says the mispricing looks particularly acute in the US, with incoming Fed Chair Kevin Warsh’s perceived bias toward looser policy possibly capping money markets’ rate-hike bets.

Article content

“Market-implied US inflation is a little low, given the strong growth data we’re seeing, combined with the energy price hit,” he said, adding it “doesn’t make any sense to us” that markets barely expect Fed hikes, even when bond yields have risen, risk assets are at record highs and inflation expectations have edged up.

Article content

Still, Riddell believes that markets have gone too far in pricing rate increases in some regions particularly in the euro area, Britain, Australia, Canada and Norway. He has moved from holding an “aggressive underweight” on nominal bonds in those markets into a “moderate overweight,” focusing on maturities up to 10 years, which he sees as attractively priced.

Article content

Meanwhile inflation risks also look underpriced across Asia, particularly in Thailand and Japan, given their reliance on Middle Eastern energy supplies, according to Riddell.

Article content

“In the West we’re not seeing much evidence of it hitting growth or even inflation that much, but in Asia you are absolutely seeing this,” he said. “What we would expect to have happened is that Asian rates should be selling off quite aggressively.”

Article content

—With assistance from James Hirai and Georgia Hall.

Article content

English (US)

English (US)